Infrared Detectors: Technology Landscape and Market Trends

2025-07-03

Key Words:Infrared detectors

An infrared detector is a transducer that converts infrared radiation signals into measurable electrical signals. Classifications are as follows:

1. By Energy Conversion Principle

· Thermal-sensitive Detectors (e.g., microbolometers, thermopiles, pyroelectric detectors): Rely on thermal effects of infrared radiation, suitable for broad-spectrum detection without wavelength selectivity.

· Photon-sensitive Detectors (e.g., photovoltaic, photoconductive, photoelectromagnetic, photoemissive detectors): Operate via photoelectric effects, requiring specific wavelength ranges and often cooling for optimal performance.

2. By Operating Temperature

· Uncooled Detectors: Operate at room temperature, ideal for low-power, portable applications.

· Cooled Detectors: Require cryogenic cooling (e.g., liquid nitrogen) to minimize thermal noise, critical for high-sensitivity scientific/military use.

3. By Spectral Range

· Near-infrared: 0.78–1.4 µm

· Short-wave infrared (SWIR): 1.4–3 µm

· Mid-wave infrared (MWIR): 3–8 µm

· Long-wave infrared (LWIR): 8–15 µm

· Far-infrared: 15–1000 µm

Thermal-sensitive infrared detectors have become mainstream in civilian applications such as consumer electronics, automotive systems, and industrial monitoring due to their cryogen-free operation and cost efficiency. Chinese manufacturers, through sustained technological accumulation, have achieved leapfrog development, now accounting for half of global infrared detector shipments and reshaping the industry landscape. Photon-sensitive infrared detectors play a pivotal role in high-end sectors like national security, military equipment, and aerospace, representing strategic technologies.

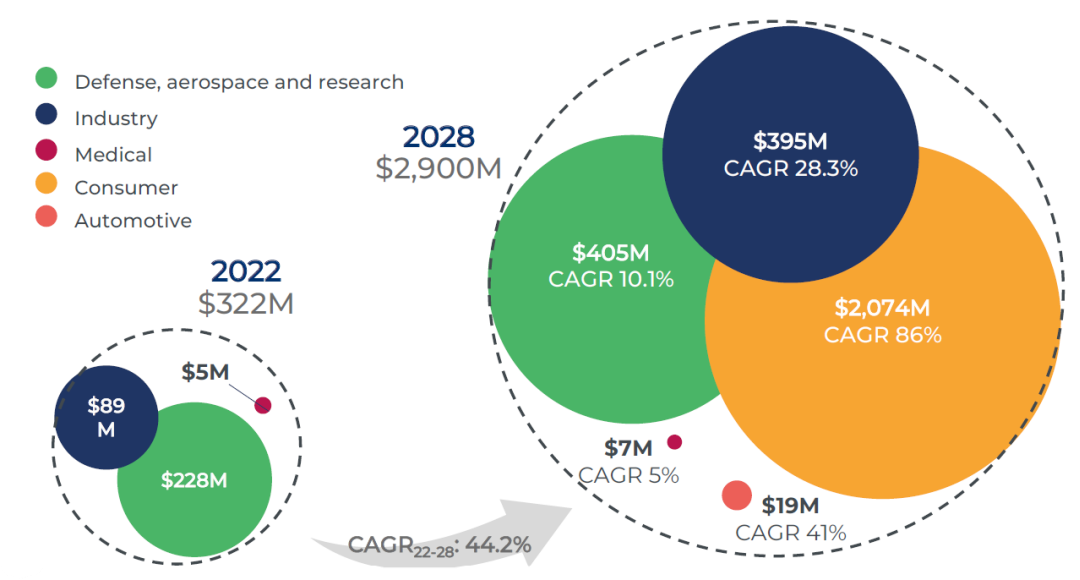

Current demand for SWIR (Short-Wave Infrared) detectors is dominated by defense and aerospace sectors, while industrial monitoring, consumer electronics, and automotive applications are emerging as high-growth segments. According to Yole reports:

· Global SWIR detector shipments are forecast to scale from 11,000 units in 2022 to 108 million by 2028, with the SWIR camera and module market valued at $2.9 billion.

· Consumer electronics will lead growth with an 86% CAGR, outpacing other verticals.

Key SWIR detector technologies include:

· Indium gallium arsenide (InGaAs)

· Quantum dots (QDs)

· Germanium-silicon (GeSi)

This exponential growth reflects expanding use cases in night vision, industrial quality control, smartphone imaging, and autonomous driving—highlighting SWIR technology's transition from niche defense applications to mainstream commercial adoption.

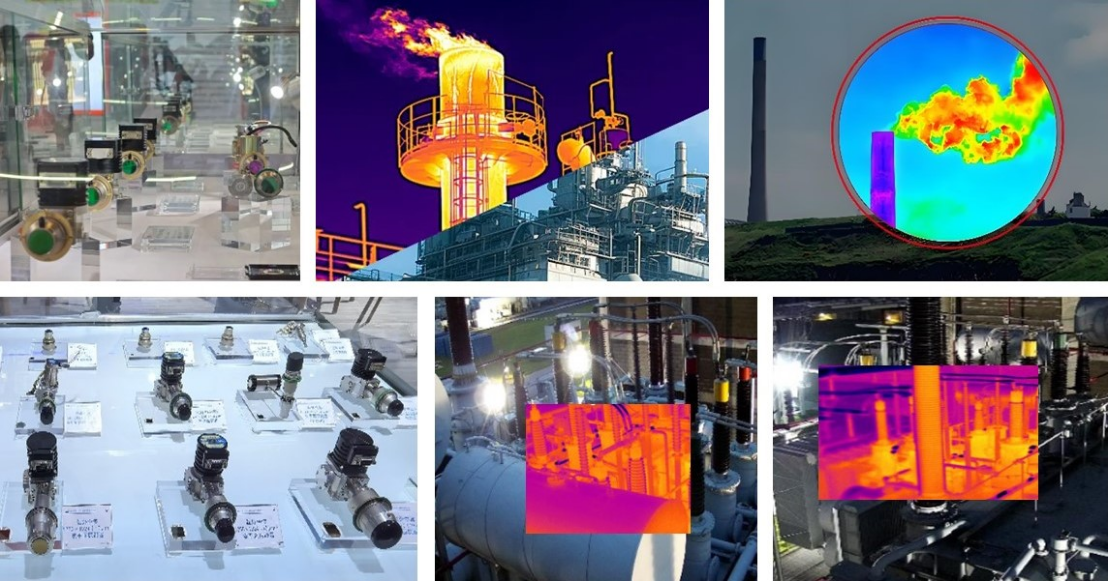

MWIR detector demand currently concentrates on defense applications, with emerging uses in gas detection, industrial monitoring, and meteorological sensing. Primary MWIR technologies include mercury cadmium telluride (HgCdTe), Type-II superlattices (T2SL), and quantum dots.

Chinese MWIR detector manufacturers have proliferated, achieving continuous breakthroughs. HgCdTe MWIR detectors are leaded by Chiptron, Vital Optics, and others. T2SL detectors are developed by KT photonics, Tegon, Raytron, and many more, while XIinIR Tech leads in quantum dot variants.

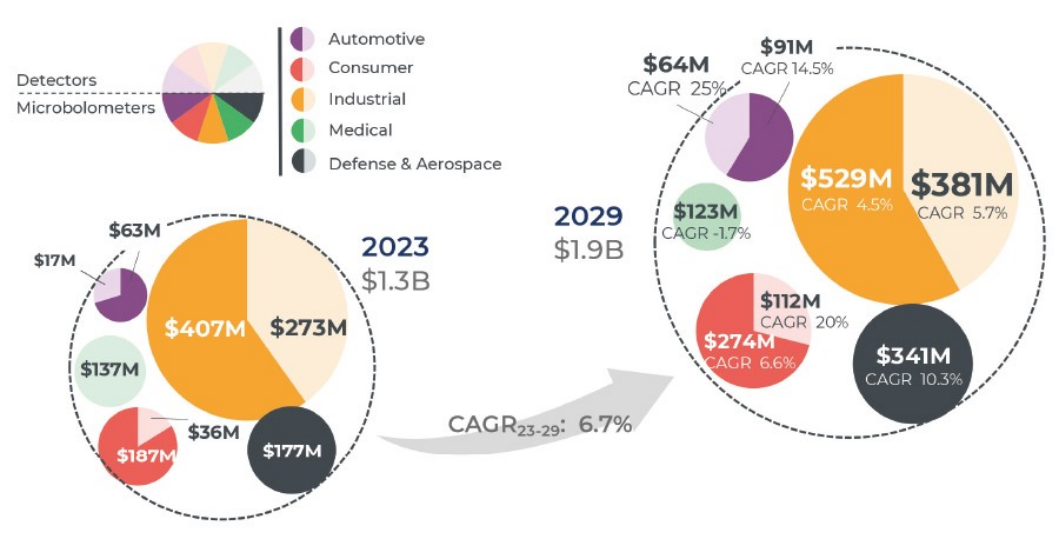

China's thermal-sensitive LWIR (Long-Wave Infrared) detector supply chain has reached full maturity, supported by a robust ecosystem of manufacturers and technology developers. Yole Group projects the global thermal detector market will grow from $1.3 billion in 2023 to $1.9 billion by 2029, driven by expanding civilian and defense applications. In contrast, photon-sensitive LWIR detectors remain cost-prohibitive and require cryogenic cooling, limiting their use to high-end defense and aerospace sectors.

This comprehensive ecosystem demonstrates China's dual-track strategy: mass-producing affordable thermal detectors while advancing cutting-edge photon-sensitive technologies for strategic applications. The infrared industry continues to evolve through material innovations and cross-sector adoption, from smartphone integration to space exploration systems.